Table of Content

You can then click on "Amortization schedule" to show the section detailing the exact amounts being applied to principal and interest each month. In terms of age, 30 percent of homeowners age 40 to 49 said they planned to prepay their mortgage loan, the largest percentage of any age group. If you prepay your Home Loan, you save Rs. 97,390 of interest you would have paid. If you prepay that Personal Loan you will save Rs. 1,45,524. So, it actually makes sense to prepay your Personal Loan, rather than your Home Loan. The only thing I feel is under represented is the financial freedom that comes with having your largest bill payed off.

Our friend has offered to loan 5.5 lacs at 5.5%. Is it benefecial to avail the opportunity and pre-close the home loan also taking into account the tax benefit we get now. Prashanth July 21, 2009I have taken loan for tenure 20 years instead opted for 8 years where my EMI became more. Is this worth than making prepayment every quarter. Most banks allow you to prepay up to a certain point without any penalty charge, so you need to ensure that your part-prepayments do not exceed this limit to avoid a prepayment penalty.

Bankrate

With the interest rate hikes over the past year I wouldn’t rule those higher interest rates in the future out for people who have to renew. This would change things considerable if not paying off the mortgage earlier. If you followed the Dave Ramsey route, in many situations, you haven't paid off your mortgage yet, have minimal investments, and should have at least some emergency savings.

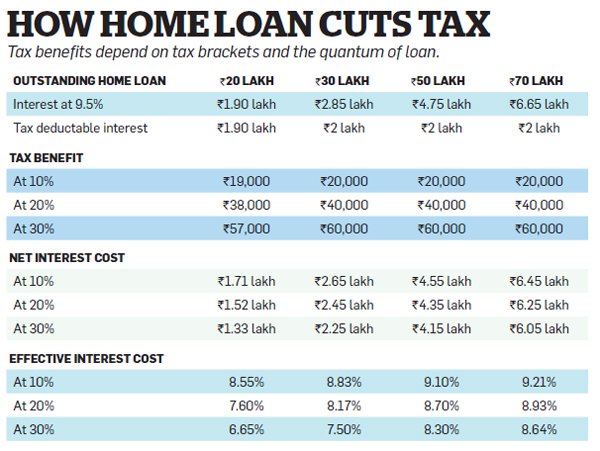

With respect to the principal amount of your loan, you can repay as much as you want without it affecting your tax exemption. There are no restrictions on this and it has no relation to your income tax filing. Vasan July 11, 2011we have taken a home loan of 8.65 lacs for 9 years at 9.5%. Now we have 7 lacs outstanding with balance 78 emi.

Top Fund Houses

Of course, there are taxes on investment gains as well, so it’s somewhat awash. Granted, you can invest tax-free depending on the investment vehicle, and grow your investments now as opposed to later. Please note that I’m not suggesting there is no way investing and keeping a mortgage can work.

There are lots of 10 year periods that don’t meet that assumption. Granted, Suzie’s return at 3.25% was guaranteed, but Ivan’s risk pays off huge. Those arguing in favor of Suzie are simply arguing out of ignorance. In addition, you’ve lost all of the possible gains during the 15 year period. Why is it that most people assume that the stock market is the only alternative that’s very limited thinking.

Savings Rates Are Terrible

For me, the only valid reason to completely pay off your mortgage at the current interest rates is that you have retired. Even then, depending upon your investments and net worth, it still might not make sense. The problem with putting most of your money into your home comes down to asset allocation. As we've found during the housing bubble, too many people had too much equity in their primary residence.

And if you actually have money or liquid assets set aside, you can use it for the down payment on the subsequent properties, instead of having it locked up in one home. There’s no rule for how much you need to pay other than your payment due. I get it though, there’s the emotional element. Some folks like the idea of being debt-free, for better or worse, financially. So if there was ever a loan to hold onto, a mortgage would be it, especially with rates where they’re at now. Let’s consider a hypothetical $250,000 loan amount tied to a 30-year fixed mortgage set at 3%.

What is the best time to Prepay your Home loan?

If you do not have sufficient contingency fund, then you can avoid Home Loan prepayment and use the fund for making bigger contingency corpus. Ranbir June 1, 2011This is a risky proposition. If your mutual funds do not yield the promised rate of return , you will face a double whammy.

Spreads between range around 0.75% difference, another error of the author. Making assumptions about future of the stock market’s gains is reckless and a little misguided. You still will have expenses now granted not as much with a mortgage but it is still possible to lose your home. I like the no debt, and buying a reasonable size house. The guy who wrote this is a moron and clearly works on commission for a lender. The key words he used are “historical lows” which is classic marketing technique for lenders.

You can expect taxes to go up nationally, as most municipalities have a shortfall in revenue. Let's assume both lived in their home for 15 years. Ivan comes out even farther ahead, with $357,636.18 of equity and investments versus $300,000 in home equity and no investments that Suze has.

Boomers will, by law, have to make withdrawls from retirement accounts, and sell stocks. I’m not the expert here, but we are in for changes. There are loads of reasons not to put all your money into your house, and it’s amazing that so many people here are even quoting numbers that are wrong to justify their ignorance. Best to pay cash for a small house, plant a food forest, become energy neutral and never buy anything on credit again. On average a home gains 2% a year, or slightly less than the rate of inflation.

Initially, the stocks are filtered on the basis of the size of the company and the sector of the company. The company's fundamental parameters are tested using various parameters related to inventory days, employee cost, power cost, taxation etc. Finally, the volatility in the price performance as well as the future growth prospect is viewed and accordingly the stocks are classified in various portfolios. I’m stuck at a 6.275% 40 year bullshit modification…I am pre-paying my mortgage. These young investment advisors always say “you have time to make it up” no you don’t. They are just pushing people so they can make money.

No comments:

Post a Comment